Introduction

Cards have replaced cash in many parts of the world. From online shopping and travel bookings to everyday payments, people now rely heavily on plastic or digital cards. Among these, credit cards and debit cards are the most commonly used.

While both look similar and can be used at the same places, they work in very different ways. Many people use them daily without fully understanding how they differ, which can sometimes lead to confusion or poor financial decisions.

This article explains the key differences between credit cards and debit cards, including the important concept of credit card vs debit card, in a simple, practical way. Understanding these differences helps users choose the right card for the right situation.

What Is a Debit Card?

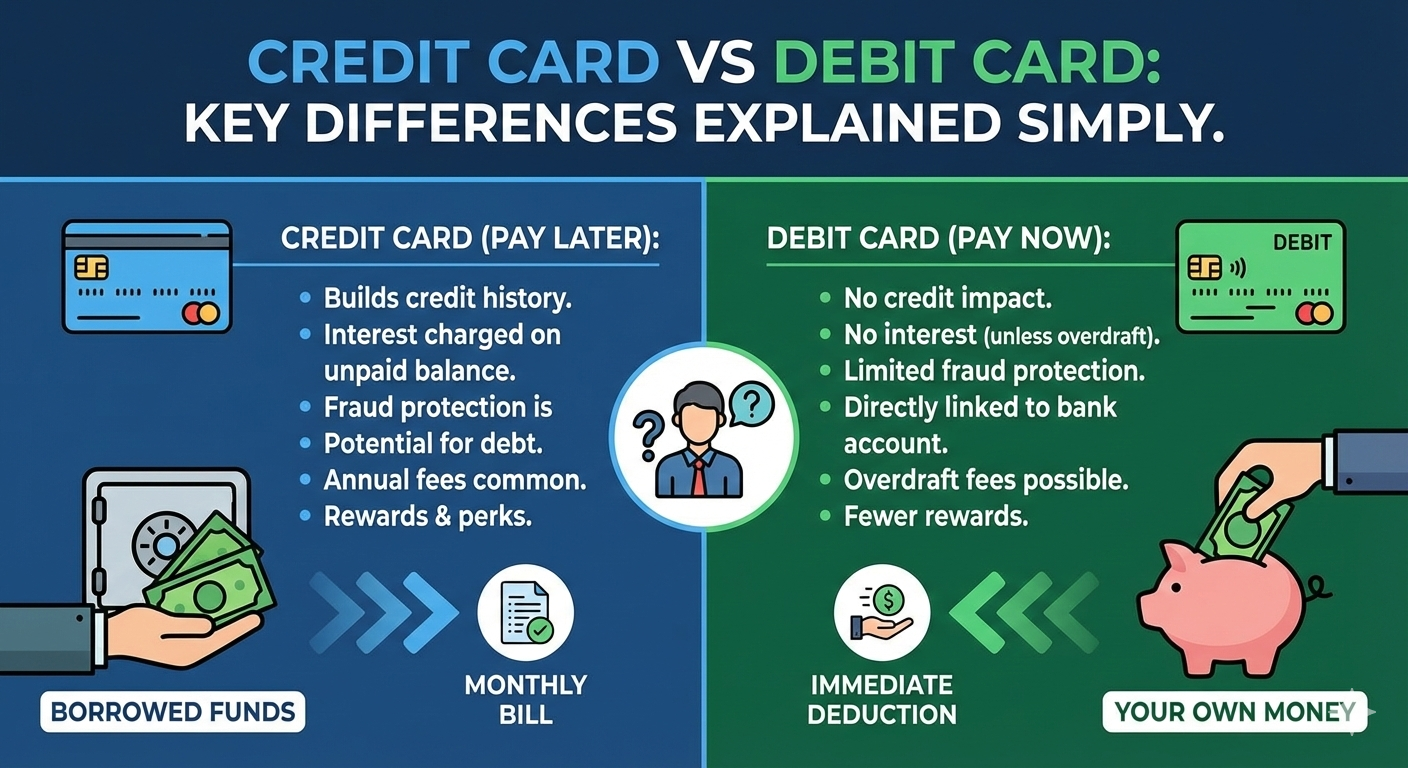

A debit card is directly linked to a bank account. When you use a debit card to make a payment, the money is taken immediately from your account balance.

In simple terms, a debit card allows you to spend only the money you already have.

Debit cards are commonly issued when a bank account is opened and are widely used for daily transactions such as shopping, bill payments, and ATM withdrawals.

What Is a Credit Card?

A credit card allows you to borrow money from a financial institution up to a fixed limit. Instead of using your own funds immediately, you use the bank’s money and repay it later.

Credit cards operate on a billing cycle. All transactions made during a cycle are added to a statement, and the user is expected to repay the amount by a specified due date.

If the full amount is paid on time, there is usually no additional cost. If not, interest charges may apply.

Core credit card vs debit card

The main difference comes down to where the money comes from.

- A debit card uses your own money

- A credit card uses borrowed money

This fundamental difference affects how each card should be used and managed.

Source of Funds

With a debit card, funds are withdrawn directly from your bank account. If your account balance is low, the transaction may be declined.

With a credit card, funds come from a pre-approved credit limit. You can make purchases even if you do not currently have the cash, as long as you stay within that limit.

Impact on Spending Habits

Debit cards naturally encourage controlled spending because users can only spend what they have.

Credit cards offer more flexibility but require discipline. Since the payment is delayed, it can be easy to overspend if usage is not monitored carefully.

Understanding this difference is important for managing personal finances responsibly.

Billing and Repayment

Debit card transactions are settled instantly. There is no repayment process because the money is already deducted.

Credit cards involve a repayment system:

- Transactions are added to a monthly statement

- A due date is set

- Users can pay the full amount or a minimum amount

Paying the full amount avoids extra charges, while partial payments may attract interest.

Interest and Charges

Debit cards generally do not involve interest charges because no money is borrowed.

Credit cards may involve:

- Interest if balances are not paid in full

- Late payment fees

- Other service charges depending on usage

This makes it important for credit card users to understand terms and repayment schedules.

Effect on Credit History

Debit card usage does not affect credit history. Since no borrowing is involved, banks do not track debit card usage for credit scoring.

Credit card usage, on the other hand, plays a role in building or impacting credit history. Responsible usage, such as timely payments, can help establish a positive credit record. Missed payments can have the opposite effect.

For individuals planning future borrowing, understanding this distinction is important.

Security and Fraud Protection

Both debit and credit cards offer security features, but their impact differs.

Debit cards expose personal bank funds. If fraud occurs, the user’s own money is temporarily at risk until the issue is resolved.

Credit cards offer an added layer of protection because transactions involve borrowed funds. Disputes are often easier to manage, and users may not lose immediate access to their own money.

Online and International Usage

Debit cards are widely accepted online, but some transactions may require additional verification.

Credit cards are often preferred for:

- Online purchases

- Travel bookings

- Hotel reservations

- International transactions

This is because they provide flexibility and are accepted globally across many platforms.

Rewards and Benefits

Debit cards usually focus on basic transaction functionality and convenience.

Credit cards may offer additional features such as:

- Reward points

- Cashback

- Travel-related benefits

These benefits vary by card and issuer, but they are designed to encourage usage.

Which Card Is Better for Daily Use?

For everyday spending, debit cards are often suitable because they promote budget control and simplicity.

Credit cards can be useful for:

- Planned expenses

- Emergencies

- Situations requiring delayed payment

The best approach is not choosing one over the other, but understanding when to use each responsibly.

Common Misunderstandings

Many people assume credit cards are risky and debit cards are always safer. In reality, both tools have their place.

Problems usually arise not from the card itself, but from how it is used. Awareness and discipline are more important than the type of card.

Choosing the Right Card for Your Needs

The choice depends on:

- Spending habits

- Financial discipline

- Short-term and long-term goals

For beginners, starting with a debit card helps build spending awareness. Credit cards can be introduced later with proper understanding and control.

Conclusion

Credit cards and debit cards serve different purposes, even though they may look similar and be used in similar places.

Debit cards offer simplicity and control by using your own funds. Credit cards provide flexibility and short-term financial convenience but require responsible usage.

When selecting between a credit card and a debit card, it is essential to consider your financial habits and goals. A debit card allows for immediate access to available funds, promoting budget management and reducing the risk of debt. In contrast, a credit card can enhance financial flexibility, enabling users to make larger purchases while building credit history, provided they adhere to disciplined repayment practices. Ultimately, the decision should align with individual financial strategies and lifestyle needs.