Introduction

At some point in life, most people come across the idea of borrowing money. It could be to buy a home, purchase a car, pay for education, or manage an unexpected expense. This is where loans come into the picture.

Loans are a common financial tool used across the world. While the word “loan” sounds straightforward, many people do not fully understand how loans work, the different types available, or the responsibilities involved.

This article explains what a loan is, how loans work, the major types of loans, and what borrowers should know before taking one.

What Is a Loan?

A loan is a financial arrangement where a lender provides money to a borrower with the expectation that the amount will be repaid over time. In most cases, repayment includes the original amount borrowed along with additional charges, usually called interest.

Loans are provided by banks, financial institutions, and other lending organisations. The terms of a loan clearly state how much must be repaid, how long repayment will take, and the conditions involved.

Simply put, a loan allows people to access funds they may not have immediately, while spreading repayment over a period of time. What Is a Loan

How Loans Work

Although loan products vary, the basic loan process remains similar across most types.

Application

The borrower applies for a loan by providing basic details such as income, purpose of the loan, and personal information. This helps the lender understand the borrower’s request.

Evaluation and Approval

The lender reviews the application to assess eligibility. This evaluation may consider factors such as income stability, repayment capacity, and credit history.

Disbursement

Once approved, the loan amount is provided to the borrower either as a lump sum or in stages, depending on the loan type.

Repayment

The borrower repays the loan over time, usually through regular instalments. These instalments include a portion of the principal amount and interest.

Understanding this structure helps borrowers manage loans more effectively.

Why People Take Loans

Loans are taken for various reasons, including:

- Purchasing property or housing

- Buying vehicles

- Funding education

- Covering personal or medical expenses

- Supporting business or self-employment needs

Loans make it possible to handle large expenses without waiting years to save the full amount.

Types of Loans

Loans can be broadly classified based on purpose and structure.

Personal Loans

Personal loans are used for general expenses such as travel, emergencies, or personal needs. They are usually unsecured, meaning they do not require collateral.

Because there is no security involved, these loans may have higher interest compared to secured loans. What Is a Loan

Home Loans

Home loans are used to purchase, construct, or renovate residential property. These loans typically have long repayment periods.

The property itself often acts as security for the loan. Due to the long-term nature and security involved, home loans usually have lower interest rates compared to other loans.

Car Loans

Car loans are designed to finance the purchase of new or used vehicles. The vehicle usually serves as collateral.

Car loans generally have shorter repayment periods compared to home loans and are structured to match the expected life of the vehicle. What Is a Loan

Education Loans

Education loans help fund academic or professional education expenses. These loans may cover tuition fees, living expenses, and study-related costs.

Repayment often begins after the education period is completed, allowing borrowers time to establish their careers. What Is a Loan

Business Loans

Business loans are used to start, expand, or manage a business. These loans may be secured or unsecured depending on the lender and business profile.

They support operational needs, equipment purchases, or expansion plans. What Is a Loan

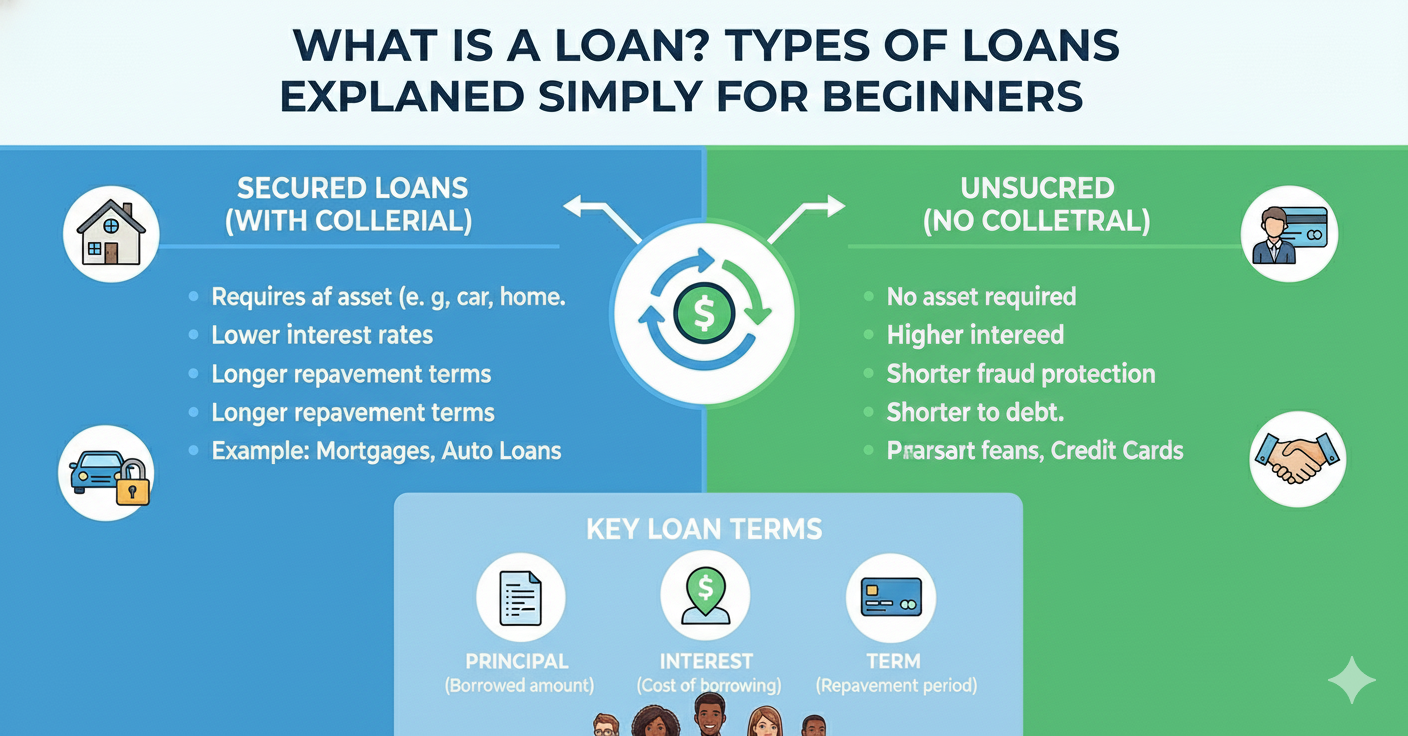

Secured vs Unsecured Loans

Loans can also be classified based on whether they require collateral.

Secured Loans

Secured loans require the borrower to provide an asset as security. Examples include home loans and car loans.

Because the lender has security, these loans often have lower interest rates and longer repayment periods.

Unsecured Loans

Unsecured loans do not require collateral. Personal loans are a common example.

Since the lender takes on more risk, unsecured loans often come with higher interest and stricter eligibility requirements. What Is a Loan

Interest and Loan Costs

Interest is the cost of borrowing money. It is calculated based on the loan amount and repayment period.

Loan costs may include:

- Interest charges

- Processing fees

- Late payment charges

Understanding these costs helps borrowers plan repayments and avoid surprises. What Is a Loan

Repayment Structure

Loans are usually repaid through instalments over a fixed period. These instalments are often called EMIs or monthly payments.

Each instalment includes:

- A portion of the original loan amount

- Interest for the period

As the loan progresses, the interest portion generally reduces while the principal portion increases.

Factors That Affect Loan Approval

Several factors influence whether a loan is approved and on what terms.

Common factors include:

- Income and employment stability

- Existing financial commitments

- Credit history

- Loan amount and duration

Lenders use these factors to assess repayment ability and risk. What Is a Loan

Benefits of Taking a Loan

When used responsibly, loans offer several benefits.

- Enable large purchases without long delays

- Spread expenses over manageable payments

- Support education and career growth

- Help manage emergencies

Loans can act as financial tools when aligned with clear goals and repayment capacity.

Risks and Responsibilities

Loans also involve responsibilities and risks.

- Long-term repayment commitments

- Interest costs over time

- Impact on credit history if payments are missed

Borrowers should carefully evaluate their ability to repay before taking a loan. What Is a Loan

Common Misunderstandings About Loans

Some people view loans as harmful by default, while others underestimate their impact. The reality lies in balance.

Loans are neither good nor bad on their own. Their outcome depends on:

- Purpose

- Planning

- Discipline in repayment

Awareness reduces financial stress and improves decision-making.

Using Loans Wisely

Responsible loan usage includes:

- Borrowing only what is needed

- Understanding terms clearly

- Planning repayments in advance

- Avoiding unnecessary borrowing

These habits help ensure loans support goals rather than create problems. What Is a Loan

Loans and Financial Awareness

Learning about loans improves overall financial literacy. Understanding borrowing builds confidence and reduces dependence on guesswork.

As financial systems grow more complex, basic loan awareness becomes essential for everyday decision-making.

Conclusion

Loans are a widely used financial tool that help individuals and businesses manage large expenses and achieve important goals.

Understanding what a loan is, how different loans work, and the responsibilities involved allows borrowers to make informed decisions. When approached with clarity and planning, loans can support progress rather than create burden.

Financial awareness begins with understanding the basics, and loans are an important part of that foundation. What Is a Loan